What GTA Crypto Investors and Traders Need to Report to the CRA

Cryptocurrency tax rules Canada 2026 guide by Easy Tax Canada, accountants in Mississauga and Brampton

Cryptocurrency is not a tax-free grey area in Canada, and the CRA has made that increasingly clear. Whether you hold Bitcoin, Ethereum, or any other digital asset, every disposal is a potential taxable event. Here is how crypto is actually taxed in 2026, and where we see GTA investors make the most costly mistakes.

Crypto Is Property, Not Currency

The CRA treats cryptocurrency as a commodity, similar to gold, rather than as currency. This means that buying and simply holding crypto is not taxable, but almost any other action, selling it, trading it for another coin, spending it, or gifting it, triggers a disposition that must be reported.

Capital Gains vs. Business Income

This is the single most important distinction in crypto taxation. If your activity is classified as investing, only 50% of your gain is taxable, exactly like selling stocks. If the CRA considers your activity business-like, such as frequent, high-volume trading, the full profit is taxable as business income at your marginal rate, which can mean paying tax on double the amount.

- Factors that point toward capital gains: infrequent transactions, long holding periods, and buying with the intention of long-term investment.

- Factors that point toward business income: high transaction frequency, short holding periods, specialized trading knowledge, and significant time spent trading.

- There is no bright-line test. The CRA and the courts look at your overall pattern of activity, not any single factor.

What Counts as a Taxable Event

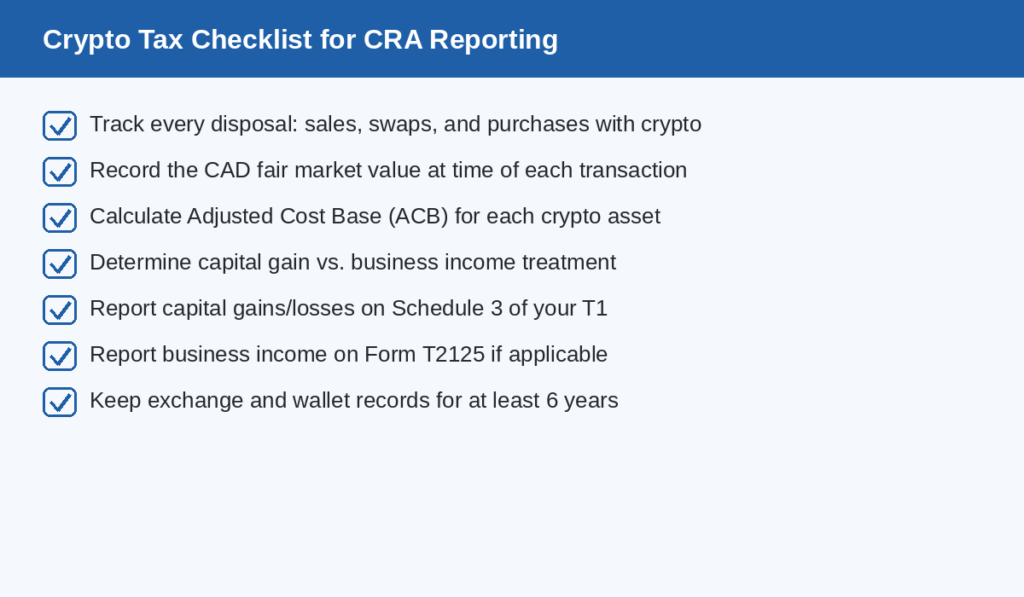

Checklist for reporting cryptocurrency taxes to the CRA in 2026, Easy Tax Canada

- Selling crypto for Canadian dollars.

- Trading one cryptocurrency for another, this is treated as two transactions, a disposal and a purchase.

- Using crypto to pay for goods or services.

- Gifting crypto to someone else, valued at fair market value on the date of the gift.

- Earning crypto through staking, mining as a business, or being paid for services, generally treated as income at the time received.

Calculating Your Adjusted Cost Base (ACB)

The CRA requires the adjusted cost base method for calculating gains and losses. If you purchased the same cryptocurrency at different times and prices, you average the cost across all units you hold. For example, buying 1 ETH at $2,400 and another at $3,100 gives an ACB of $2,750 per ETH, which is then used to calculate your gain or loss on any future sale.

| Keep detailed records for every wallet and exchange you use: dates, CAD values at time of each transaction, and fees. The CRA has information-sharing arrangements with Canadian exchanges, and reconstructing years of transaction history after the fact is far more expensive than tracking it as you go. |

How to Report Crypto on Your Return

Capital gains and losses are reported on Schedule 3 of your T1 personal return. If your activity is classified as business income, you report it on Form T2125 instead, and may be able to deduct related expenses such as trading fees and platform costs. Corporations report crypto activity through their T2 return.

Final Thoughts

Crypto tax reporting in Canada is not optional, and the classification of your activity, capital gains or business income, has a major impact on how much tax you actually owe. If you have unreported crypto activity from previous years, addressing it proactively is almost always better than waiting for the CRA to reach out first.

| Need Help With This? Talk to Easy Tax Canada. Our team is led by a former CRA Auditor and Collections Officer with over 15 years of experience, backed by CPAs who know the Canadian tax system inside and out. We help individuals, self-employed professionals, and small businesses across Mississauga, Brampton, and the Greater Toronto Area file accurately, plan ahead, and stay CRA-compliant year-round. Visit easytaxcanada.com to book a consultation or explore our blog for more tax guidance. |